The paper instruments popular for transfer of funds are cheques and demand drafts. There are also systems which provide you

paperless transactions. A customer just has to give some details for the funds transfer to a bank. The beneficiary or the drawee of

payment does not have to move to a bank branch for depositing the paper instruments. The one transferring funds can also initiate the

process at home using internet banking. Transactions are secured.

The two popular systems NEFT and RTGS for funds transfer are explained in this article.

National Electronic Funds Transfer (NEFT) is a nation-wide payment system facilitating one-to-one funds transfer. Under this

Scheme, individuals, firms and corporates can electronically transfer funds from any bank branch to any individual, firm or corporate

having an account with any other bank branch in the country participating in the Scheme.

It is an electronic fund transfer system that operates on a Deferred Net Settlement (DNS) basis which settles transactions in batches.

By the word ‘batches’ it mean that instructions received for transferring the money will not be done as soon the request is received. So,

the settlement takes place with all transactions received till the particular cut-off time.

From July 10, 2017 settlements of fund transfer requests in NEFT system is done on half-hourly basis. There are twenty three half-hourly settlement batches run from 8 am to 7 pm on all working days of week (Except 2nd and 4th Saturday of the month).This can be explained by an example: If you submit your request of transfer of payment at say, 1: 10 PM on any of the week day, the settlement will get started at next batch i.e. 1:30 PM to 2 PM batch along with all the requests which were submitted in the 1 PM to 1:30 PM batch.

Not every bank can transfer or receive money through NEFT system. For this the bank should be NEFT enabled. A list of NEFT

enabled bank branches is available on RBI website, and also you can obtain this information from your bank.

There is no minimum or maximum limit for opting for a NEFT payment system. However, if you do not have an account in a bank,

then you can only transfer up to Rs 50,000 per transaction.

NEFT payment system is also available to transfer funds to Nepal under Indo-Nepal Remittance Facility scheme. While

transferring funds to Nepal, there is a maximum limit of Indian Rupees 50,000 and the beneficiary in Nepal will get them in

Nepalese Rupees. Any customer of bank or walk-in-customer can do a transfer of up to Rs 50,000 to Nepal.

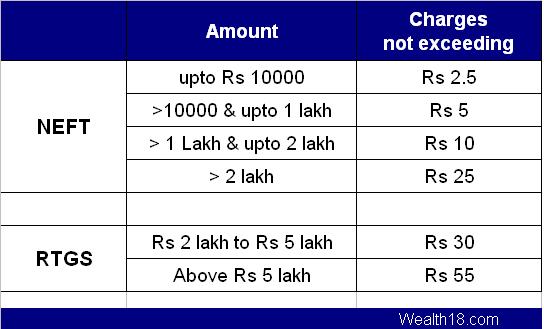

Banks charge Processing Charges / Service Charges for NEFT transaction.

Details you need to give while requesting for NEFT transfer:

Your bank account number with bank, so that bank can debit amount from that account.

The amount to be remitted.

Beneficiary’s name.

Beneficiary’s bank’s and branch’s name (Bank branch should be NEFT enabled).

Beneficiary’s account number.

IFS code of bank branch of beneficiary. (IFS Code of all bank branches is available on RBI website ,in the users bank passbook.)

The Indian Financial System Code (IFS Code or IFSC) is an alphanumeric code that facilitates electronic fund transfer in India. A code uniquely identifies each bank branch participating in the NEFT , RTGS and IMPS.

The IFSC is an 11-character code with the first four alphabetic characters representing the bank name, and the last six characters (usually numeric, but can be alphabetic) representing the branch. The fifth character is 0 (zero) and reserved for future use. Bank IFS Code is used by the NEFT & RTGS systems to route the messages to the destination banks/branches. The format of the IFS Code is shown below.

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 |

|---|---|---|---|---|---|---|---|---|---|---|

| Bank Code | 0 | Branch Code | ||||||||

RTGS

The acronym ‘RTGS’ stands for Real Time Gross Settlement. Real Time means that the processing of instructions start at same time

when they are received and not at some later time. Gross settlement means that the settlement of funds transfer instructions occurs

individually (on an instruction by instruction basis).

Not every bank can transfer or receive money through RTGS system. For this the bank should be RTGS enabled. A list of

RTGS enabled bank branches is available on RBI website, and also you can obtain this information from your bank.

So this is in contrast with the NEFT system in which settlements take place in batches.

In contrast with NEFT system, there is a minimum limit of Rs 2,00,000 to be transferred through RTGS. Though there is no

maximum limit.

Banks charge Processing Charges / Service Charges for RTGS transaction.

Details you need to give while requesting for RTGS transfer:

Your bank account number with bank, so that bank can debit amount from that account.

The amount to be remitted.

Beneficiary’s name.

Beneficiary’s bank’s and branch’s name (Bank branch should be NEFT enabled).

Beneficiary’s account number.

IFS code of bank branch of beneficiary.

bank charges for outward transactions:

Inward transaction– no charge to be levied.

# ARCHANA